IRS Tax Fraud Whistleblower

Since 2006, the IRS has maintained the IRS Whistleblower Office. The IRS Whistleblower Office assists with the process of handling claims by tax fraud whistleblowers, including the payment of rewards to those who blow the whistle on tax evasion. The Whistleblower Office and whistleblower rewards were created by the 2006 Tax Relief and Health Care Act.

Following the success of the False Claims Act in encouraging whistleblowers to report fraud, the Tax Relief and Health Care Act set up rewards to those that disclose cases of knowing tax fraud. While the False Claims Act had additional whistleblower rewards added in the 1980s, it does not allow for claims regarding tax liability and tax fraud. Now the IRS Whistleblower Office handles such claims, and those who report wrongdoing can receive up to 30% of the recovery. In 2019, the IRS awarded more than $120 million dollars to whistleblowers.

For frequently asked questions, visit our IRS Whistleblower FAQ. To learn more about IRS claims, whistleblower rewards or IRS whistleblower protections, schedule a comprehensive claims assessment with the knowledgeable lawyers of Schneider Wallace Cottrell Kim. You can contact us at 1-800-689-0024 or info@schneiderwallace.com.

Tax Relief and Health Care Act

The Tax Relief and Health Care Act of 2006 established the modern IRS tax fraud whistleblower program and its reward structure. Since 2007, the IRS has awarded nearly $1 billion to whistleblowers for their efforts in assisting tax collection. Every year, the IRS receives more than 10,000 new claims of IRS tax fraud, tax evasion, or tax underpayment. The law not only establishes potential awards for those who disclose tax fraud, but also requires by law the awarding of 15-30 percent of any applicable recovery to the whistleblower.

Major additions were made to the program by way of the enactment of the Taxpayer First Act in 2019. This law added additional protections for whistleblowers against employer retaliation. The Act also added additional required disclosures to whistleblowers, who must now receive updates on the status of claims including payments.

For more on IRS whistleblower rules, visit our IRS Whistleblower FAQ.

IRS Tax Fraud Penalties

Individuals are subject to fines of $250,000 for tax evasion, while corporations can receive fines up to $500,000. For other tax fraud crimes, penalties of $100,000 for individuals and $200,000 for entities exist.

In addition to fines, a guilty party must make tax restitution. Tax restitution is the repayment of taxes they failed to pay to state and/or federal governments. This is in addition to penalties or fines.

The costs of prosecution for tax fraud can also be charged to the guilty part in a tax evasion case, in addition to restitution and fines.

IRS Whistleblower Rewards

The Tax Relief and Health Care Act of 2006 established the modern IRS tax fraud whistleblower program and its reward structure. Since 2007, the IRS has awarded nearly $1 billion to whistleblowers as a reward for their efforts to curb tax evasion. Half of that total was awarded in just the last 3 years:

| IRS Tax Awards | FY 2017 | FY 2018 | FY 2019 |

|---|---|---|---|

| Total Claims Related to Awards | 367 | 423 | 510 |

| Total Number of Awards | 242 | 217 | 181 |

| Total IRC § 7623(b) Awards | 27 | 31 | 24 |

| Total Amounts of Awards | $33,979,873 | $312,207,590 | $120,305,278 |

| Proceeds Collected | $190,583,750 | $1,441,255,859 | $616,773,127 |

| Awards as a Percentage of Proceeds Collected | 17.8% | 21.7% | 19.5% |

Mandatory Awards (Section 26 USC § 7623(b)):

The law requires the IRS to give an award of 15 to 30% of the fraud recovery or tax underpayment under section 26 USC § 7623(b), if:

- The IRS collects tax underpayments resulting from the action or related actions;

- The amount disputed exceeds $2 million (and if an individual and not an entity, the defendant earned at least $200,000 one year in income); and

- The IRS acts upon the tip from a whistleblower.

The Tax Relief and Health Care Act differs from the False Claims Act in that qui tam lawsuits are not allowed under the former. A qui tam lawsuit allows an individual to proceed on behalf of the government, potentially winning a case even if the government elects to not join the lawsuit. For IRS tax fraud and tax underpayment, the IRS must carry the action forward and individuals cannot proceed with a lawsuit on their own.

Discretionary Awards (Section 26 USC § 7623(a)):

If a case does not meet the criteria above for a mandatory award, it is still possible for a whistleblower to receive an award. Discretionary awards are possible for any case that results in “detecting underpayments of tax or bringing to trial and punishment persons guilty of violating the internal revenue laws”. The maximum award for discretionary awards is 15 percent of the tax recovery.

Award Denial or Reduction:

The IRS can reduce an award by 10% or eliminate a reward in these conditions:

- The whistleblower is also an individual who planned and initiated the actions that lead to the underpayment of tax;

- The whistleblowers information is sourced from a judicial or administrative hearing, government report, audit, or investigation, or is sourced from public information in the news.

If the IRS determines the source of the information was a public hearing or public information in the news, that can result in award reductions. Being a party to the fraud or underpayment including initiation and planning can also result in a reduced award. A whistleblower that was party to a tax fraud is not necessarily barred from a recovery however, especially if the party learned of the fraud by being joined to an ongoing already planned and initiated scheme. If you have been asked to take part in an illegal tax scheme, even if you have participated in the scheme, you should contact an attorney and consider reporting the tax fraud to the IRS.

For more on IRS Whistleblower rewards, visit our IRS Whistleblower reward page.

IRS Tax Whistleblower Claims

IRS tax fraud claims are processed by the IRS based on the type of tax underpayment, fraud, or evasion. The IRS divides cases into these categories for processing and administration:

- Large Business and International (LB&I)

- Small Business and Self-Employed (SB/SE)

- Tax Exempt and Government Entities (TE/GE)

- Criminal Investigation (CI)

Large Business and International: This division is responsible for activities of taxpayers with assets of more than $10 million or international entities.

Small Business and Self-Employed: This division is responsible for activities of taxpayers who do not meet the requirements for the LB&I division.

Tax Exempt and Government Entities: This division handles claim involving charities and other exempt organizations, government entities, and pension plans.

Criminal Investigation: Tax evasion that contains elements of illegal crimes, such as a tax evasion from proceeds of an illegal product, is handled by the Criminal Investigation (CI) division. If another department determines an ongoing case involves criminal acts, it may transfer the case to the CI division.

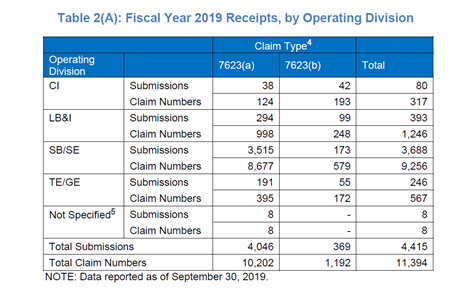

In the 2019 fiscal year, the number of cases in each division were as follows:

The IRS has received 35,626 claims over the last 3 fiscal years of 2017 to 2019, an average of nearly 12,000 claim per year. Over 500 whistleblowers received a “Claim Paid in Full” – a rate of 2 whistleblower award payments per business day of the year.

IRS Whistleblower Cases

Whistleblower 21276-13W v. Commissioner: The IRS appealed a decision of the Tax Court that, in addition to tax collections being eligible for up to 30% in awards to whistleblowers, criminal fines and civil forfeitures should also be included in the award. In the case in question, whistleblowers reported tax fraud that resulted in $20 million in tax restitution and an additional $54 million in civil forfeiture and criminal fines. The Tax Court ruled that the whistleblowers should receive a portion of the criminal fines and civil forfeiture, as well as a portion of the tax collection. In this case, that would result in nearly 4 times the potential reward, as the ensuing civil forfeiture and criminal fines was nearly 3 times the initial tax collection. The U.S Court of Appeals in the District of Columbia is currently reviewing the decision. The whistleblowers would receive as much as $13 million in addition to their $4.8 million reward.

UBS Switzerland AG: In 2007, as a result of the 2006 passing of the Tax Relief and Health Care Act, Bradley Birkenfeld famously blew the whistle on Swiss bank tax evasion. After the IRS collected $400 million in taxes, Birkenfeld was awarded 24% of the recovery – that is, $104 million. The $104 million award represents the largest award the IRS has given to a whistleblower. Birkenfeld received the award despite being a party to the scheme and himself being charged and convicted of a crime. UBS would additionally pay a $780 million fine and the whistleblower case resulted in the release of previously secret Swiss bank account information to the US government.

Tax Relief and Health Care Act Law

The law establishes a mandatory award for whistleblowers as set forth in Section 26 USC § 7623(b):

(b) Awards to whistleblowers

(1) If the Secretary proceedswith any administrative or judicial action described in subsection (a) based on information brought to the Secretary’s attention by an individual, such individual shall, subject to paragraph (2), receive as an award at least 15 percent but not more than 30 percent of the proceeds collected as a result of the action (including any related actions) or from any settlement in response to such action (determined without regard to whether such proceeds are available to the Secretary). The determination of the amount of such award by the Whistleblower Office shall depend upon the extent to which the individual substantially contributed to such action.

Whistleblower claims which fall under Section 7623(b) require a mandatory award of 15 to 30 percent of the resulting tax restitution. Discretionary awards are available under Section 7623(a) for claims that do not fit the criteria of Section 7623(b):

(a) The Secretary, under regulations prescribed by the Secretary, is authorized to pay such sums as he deems necessary for

(1) detecting underpayments of tax, or

(2) detecting and bringing to trial and punishment persons guilty of violating the internal revenue laws or conniving at the same,

in cases where such expenses are not otherwise provided for by law. Any amount payable under the preceding sentence shall be paid from the proceeds of amounts collected by reason of the information provided, and any amount so collected shall be available for such payments.

IRS Taxpayer First Act of 2019

The IRS Taxpayer First Act of 2019 (TFA 2019) provided additional protections for whistleblowers. TFA 2019 amended Section 7623 to provide protections from retaliation to IRS whistleblowers, and amended Section 6103 to require the IRS to disclose information to whistleblowers on the status and results of investigations.

The result of TFA 2019 is whistleblowers now enjoy extra employment protections and can be assured they will receive mandatory disclosures after making a claim. The Whistleblower Office revised its procedures to send notices that are required when a case has been referred for audit or examination. The Whistleblower Office will also notify the whistleblower when the taxpayer reported by the whistleblower has made a tax payment based on the whistleblower’s information. Whistleblowers can submit a request for information on the status and stage and reason for an award determination on the amount of any award made under IRC § 7623(b).

Information shared with whistleblowers is subject to confidentiality.

IRS Whistleblower Lawyer

Schneider Wallace represents whistleblowers. Schedule a consult with our whistleblower law firm for a free and private legal consultation. To speak with a lawyer regarding IRS tax fraud, contact us at 1-800-689-0024.