Media

Schneider Wallace Files ERISA Case Against John Muir Health for Excessive 403(b) Retirement Plan Fees

On March 15th, 2024, Schneider Wallace Cottrell Kim LLP filed a lawsuit in the Northern District of California against John Muir Health and its Board of Directors. The complaint alleges that John Muir Health violated their fiduciary duties under the Employee Retirement Income Security Act (ERISA).

John Muir Health, along with its Board, function both as the Plan Sponsor and the Plan Administrator. As alleged fiduciaries, they are legally obligated to act with the highest level of loyalty and prudence, solely in the interests of the participants and beneficiaries of the plan.

Alleged Failure to Meet Fiduciary Duties

The complaint alleges several instances where the defendants allegedly failed to uphold their fiduciary duties. These failures include:

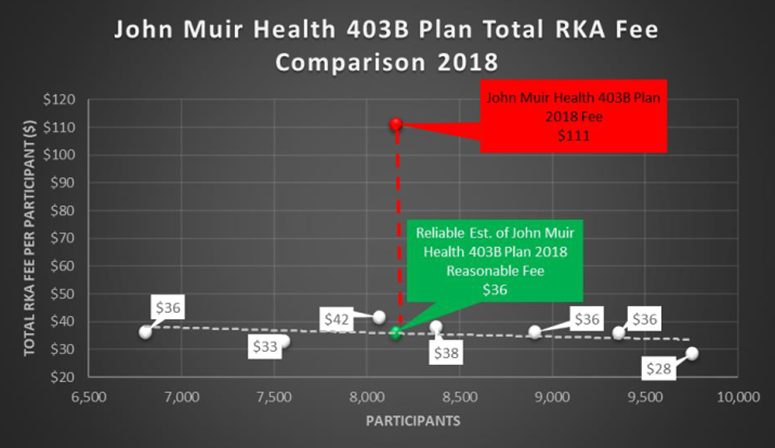

- Excessive Fees: The defendants are accused of causing the plan to pay excessive recordkeeping and administrative (RKA) fees. This was allegedly done by maintaining multiple vendors for these services—specifically Fidelity Investments Institutional Operations and Lincoln National Corporation—instead of consolidating services to achieve lower costs. Furthermore, the complaint alleges the defendants failed to effectively use their bargaining power to negotiate lower fees, despite the plan’s substantial size.

- Mismanagement of Forfeited Funds: The defendants are also accused of misusing forfeited employer contributions by allocating them towards reducing the company’s future contribution expenses rather than using these funds to reduce the administrative expenses charged to participant accounts.

These alleged actions have led to the filing of four specific counts against the defendants:

- Count I: Breach of the fiduciary duty of prudence by incurring unreasonable Total RKA fees.

- Count II: Breach of the fiduciary duty of loyalty by improperly retaining forfeited employer contributions for the company’s benefit, rather than using them to decrease participant fees.

- Count III: Breach of the fiduciary duty of prudence by failing to adequately monitor those responsible for managing the plan’s Total RKA fees.

- Count IV: Breach of the fiduciary duty of loyalty by failing to ensure proper management of forfeited funds.

Each of these counts reflects an alleged violation of specific provisions under ERISA, which mandates fiduciaries manage plans with care, skill, prudence, and diligence, while considering the best interests of the participants. Fiduciaries have a continuous duty to monitor investments and expenses and to ensure that they are reasonable and prudent.

ERISA LAW

ERISA sets out that fiduciaries must operate a plan for the exclusive purpose of providing benefits to participants and their beneficiaries, allowing reasonable expenses for administering the plan. The allegations in the filed complaint state defendants failed to adhere to these principles, by allowing the plan to incur unnecessary expenses and by prioritizing the company’s financial interests over those of the plan participants.

Ultimately, these breaches of fiduciary duty allegedly resulted in significant financial losses for the participants. The losses are manifested as lower retirement account balances due to excessive fees.

John Muir Participant Alleged Excessive Fees

The plaintiff, representing the interests of all affected class members, seeks to enforce the defendants’ liability under ERISA to compensate the plan for all losses resulting from these alleged breaches.

As stated in the complaint:

The sheer volume of nearly one hundred and fifteen (115) total investment choices for retirement investors like Plaintiff indicates that Defendants [allegedly] failed properly to monitor and evaluate the historical performance and expense of each of these funds, compare that historical performance and expense to a peer group of funds and/or even compare the three segments –comprised of Fidelity and Lincoln offerings — against one another.

This strategy chosen by Defendants [allegedly] results in the inclusion of many investment alternatives that were duplicative, that a responsible fiduciary should exclude, and unreasonably burdens Plan participants who do not have the resources to pre-screen investment alternatives in the way Defendants do.

The complaint alleges RKA fees per participant from the years 2018 to 2023 were an estimated $111-$146 per year, instead of the alleged more reasonable rates of $36. Combined with the number of participants, as high as 8,000 in some years, the result was fees and costs alleged to be approximately $600,000 per year higher than reasonable.

ERISA Law Firm

A class action allows participants, who have lost money due to excessive fees or imprudent investments, to bring a cause of action against the fiduciaries of a plan, and others. ERISA litigation is ideally served through the class action process because participants are almost always in similar positions and have suffered the same types of damages arising from the same wrongdoing. By filing as a class, the lawyers can focus discovery and case preparations on key issues that affect multiple participants and return money to all members of the plan.

If you feel you lost returns or retirement savings due to excessive fees, contact one of our offices in California, Texas, and Puerto Rico to schedule an appointment with our experienced class action lawyers. Schneider Wallace helps ERISA participants recover damages for excessive fees and imprudent investments. We are a national firm and, by partnering with local firms, we can assist clients in any jurisdiction.